Bigger Limits in 2026: How to Supercharge Your 401(k) and IRA for Real Retirement Growth

Maximize Your Retirement Savings in 2026: New 401(k) and IRA Limits Explained (And How to Make the Most of Them) – Fully Illustrated!

Checking your accounts after the holiday buzz and thinking about the year ahead—retirement planning is probably on your mind. The IRS just dropped the updated contribution limits for 2026, and there are some nice bumps that could help you supercharge your nest egg.

I've been diving into this stuff for years, and honestly, maxing out these accounts has been one of the best moves I've made. With markets still riding high from recent years and uncertainty always lurking (inflation, rates, geopolitics), locking in more tax-advantaged savings feels smarter than ever. Let's break it down simply—what's new, how to maximize, my personal predictions, and answers to questions I get all the time.

The Key 2026 Updates: Bigger Limits Mean More Opportunity

Here's the fresh numbers straight from the IRS (visualized for easy reference):

- 401(k), 403(b), and most 457 plans: Employee contribution limit jumps to $24,500 (up from $23,500 in 2025). Total with employer match can hit around $73,000.

- Catch-up for age 50+: Standard $8,000 extra, up to $32,500. Ages 60–63 get up to $11,250 super catch-up in some plans.

- Traditional/Roth IRA: $7,500 limit (age 50+: $8,600 with catch-up).

These increases are inflation-adjusted—small but powerful over time.

How to Actually Maximize in 2026: My Practical Suggestions

Visualizing the magic of compounding always motivates me—here's what steady contributions can do:

- Grab the employer match first — instant return!

- Automate increases — bump by 1–2% without feeling it.

- Roth vs Traditional? Here's a quick comparison to help decide:

Quick prediction: 2026 could see strong growth with AI/tech momentum—contribute now for potential upside (or buy low if dips hit).

Common Questions I Get (And My Honest Answers)

Q: Can I really afford to max these out? A: Start small—compounding turns it huge.

Q: Roth or Traditional? (See the visual above!)

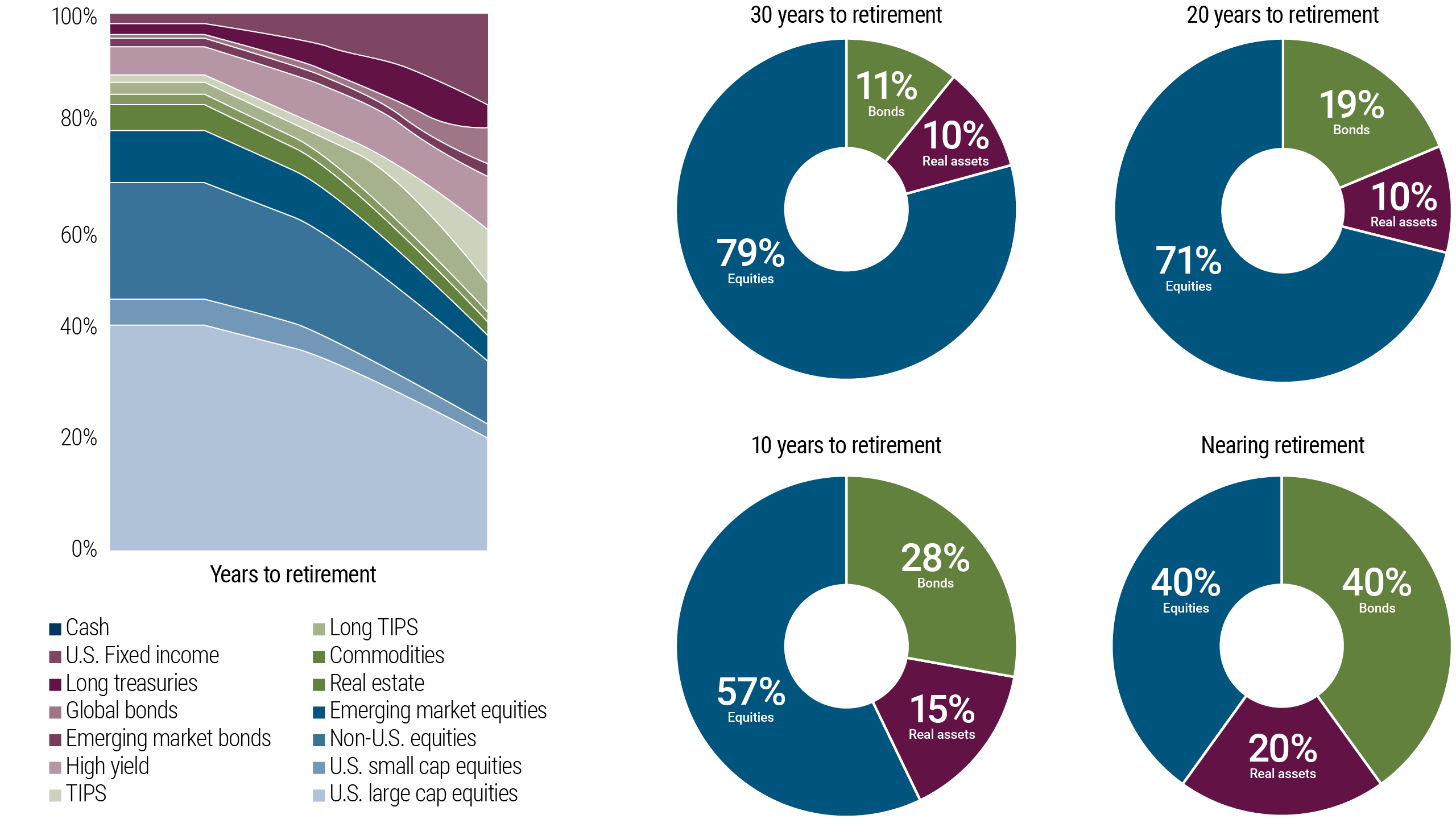

Q: Markets high—worth it? A: Yes, time in market wins. A balanced allocation helps smooth rides:

My view? These accounts are a game-changer. Aim high this year!

What about you? Bumping contributions? Biggest retirement question? Comment below—I read them all.

Important Disclaimer Just my personal take for education only. Not advice—check IRS.gov and pros. Risks apply.

Follow @MoneyWise2026 on X for more.

To a wealthy retirement, Angel from Florida

Comments

Post a Comment