How Much Do You Need to Retire Early?

Retirement Planning in 2026: How Much Do You Really Need to Retire Early? The FIRE Number That Could Change Your Life

Where the sun shines bright but the cost of living? Not so much. Imagine waking up at 45, no alarm clock, no boss — just coffee on the porch and doing whatever you want. That’s the FIRE dream (Financial Independence, Retire Early), and in 2026 it’s more real than ever… but only if you know your number.

The big question everyone asks me: “How much do I actually need to retire early?” If you guess wrong, you could run out of money or work decades longer than necessary. Let’s fix that today.

The 4% Rule: The Simple Math That’s Helped Thousands Quit Early

Category: Retirement Planning - Expat Wealth At Work

Category: Retirement Planning - Expat Wealth At WorkThis rule (backed by studies like the Trinity Study) says: withdraw 4% of your savings in year one, adjust for inflation after, and historically it lasts 30+ years with 95% success rate.

The magic multiplier? ×25 your annual expenses.

- Want $40k/year to live? $1 million nest egg.

- $60k/year? $1.5 million.

- $100k/year? $2.5 million.

But wait — if you’re retiring in your 40s, go safer with 3–3.5% (×28–33). Why? Your money needs to last 50 years, not 30. Ignore this, and a market crash early on could wipe you out.

How to Find Your Personal FIRE Number – Do This Today

- Track your real retirement expenses What will life cost without a job? Housing, food, travel, hobbies, taxes — add healthcare and inflation buffer. Most aim for 70–80% of current spending, but surprises happen.

- Subtract guaranteed income Social Security (check ssa.gov), pensions, rentals. The gap is what investments cover.

- Choose your rate 4% for moderate risk, 3% for "sleep like a baby".

- Crunch the numbers Example: Need $60k/year total, Social Security gives $24k. Gap $36k × 25 = $900k (4%) or ×33 = $1.2 million (3%).

Do this now — in 5 years, inflation could force you to save 20–30% more!

The 2026 Wake-Up Call: Why It’s Harder (And Smarter) Now

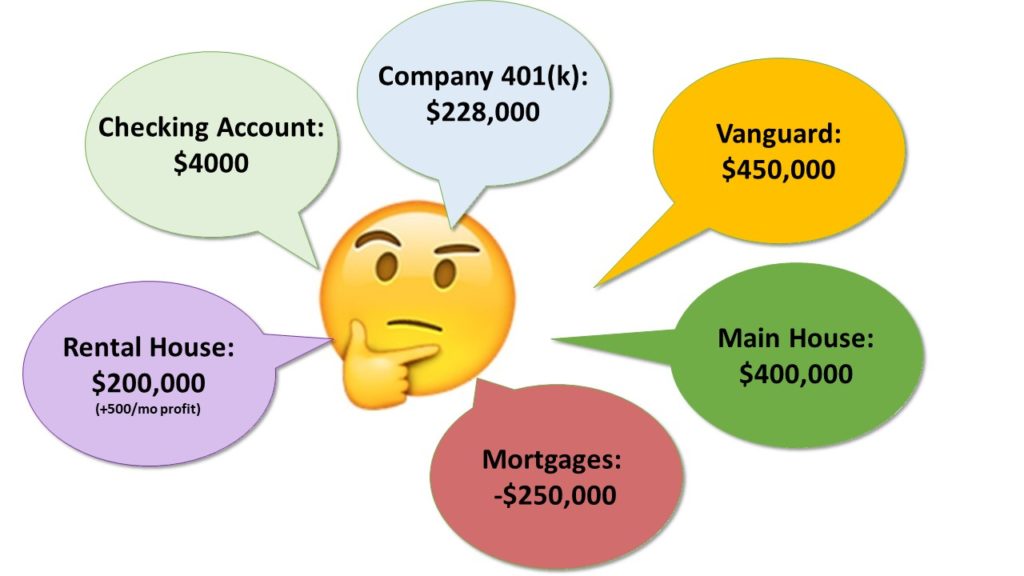

How to Retire Forever on a Fixed Chunk of Money

Inflation isn’t sleeping. Healthcare before 65 can hit $15k+/year per person. Market dips hurt more when retirement lasts decades. Taxes on withdrawals add up.

But here’s the good news: flexible FIRE folks thrive — cut spending in bad years, add side income, move smart. Start today, and compound interest does the heavy lifting. Delay? You’ll need way more each month.

How Renewable Energy Models Can Produce Misleading Indications ...

Important Disclaimer General info only — I’m not a financial advisor. Risks are real: outliving savings, crashes, rising costs. 4% rule is historical, not guaranteed. Do your research and consult a pro.

What’s your FIRE goal? Lean and free by 45? Comfortable travel life? How close are you? Comment below — let’s inspire each other!

Follow me on X @MoneyWise2026

By Angel from Florida

Comments

Post a Comment