How Much House Can You Really Afford in 2026?

How Much House Can You Really Afford in 2026? Florida Edition

You know that dream of owning a piece of paradise here in Southwest Florida — a canal home in Cape Coral, a pool house with gulf access, or just a solid spot to call your own without breaking the bank? I've been there, scrolling Zillow late at night, heart racing at listings, only to crunch the numbers and feel the reality check. How much house can you really afford in 2026, especially in Florida where everything feels extra expensive these days? Let's talk about it honestly — no sugarcoating, just real talk from someone living it.

![2905 SE 22nd Pl, Cape Coral, FL 33904 [Updated 1/30]](https://ap.rdcpix.com/eb7b7462971d7feae1dfe1b6618691bfl-m1020253471rd-w1280_h960.webp)

A little history to put things in perspective (because understanding bubbles helps avoid them). Remember the mid-2000s housing boom? Easy loans, flipping frenzy, prices skyrocketing — then 2008 crashed it all, with Florida hit hardest (foreclosures everywhere, values dropping 50%+ in places like Cape Coral). Families overextended on "affordable" McMansions got wiped out. Fast-forward to the pandemic boom: low rates + remote work flooded Florida with buyers, prices doubled in years. Now in 2026, rates have eased a bit but insurance and taxes are through the roof — making "affordability" a moving target.

Question everyone asks: "What's the golden rule for affordability?" The classic 28/36 rule: No more than 28% of gross income on housing (mortgage, taxes, insurance, HOA), and 36% on all debt. But in Florida 2026? That rule feels outdated with home insurance averaging $6,000–$10,000/year (post-hurricane spikes) and property taxes climbing fast.

Real Florida example: Median household income here ~$70,000 (2026 estimate). 28% = ~$1,960/month for housing. At 6.5% mortgage rate on a $400k home (common starter in our area): Principal/interest ~$2,500 + $800 taxes/insurance = $3,300/month — way over. Realistic affordable price? Closer to $300–$350k to stay safe.

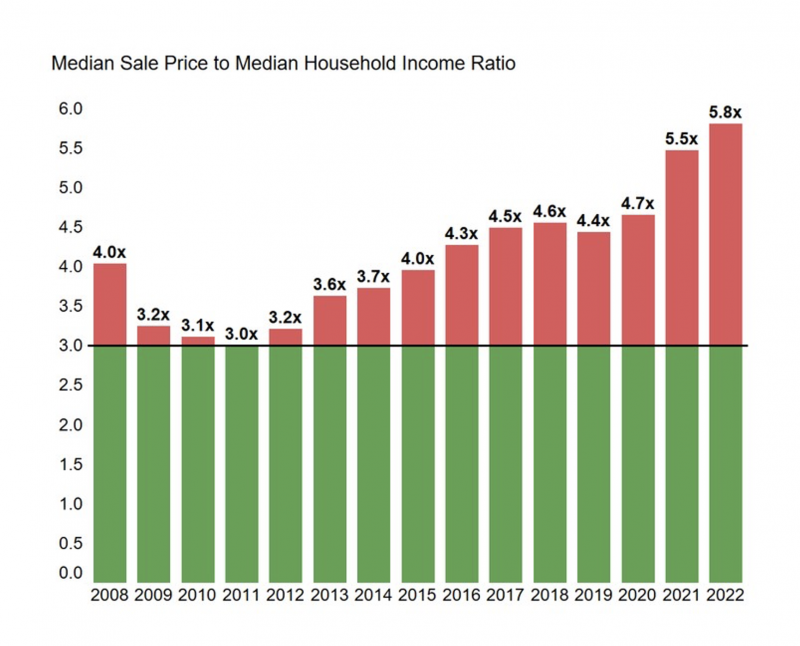

Florida's Affordability: Price vs. Income

Florida's Affordability: Price vs. Income Biggest Florida twists making it harder in 2026:

- Insurance crisis: After Ian (2022) and recent storms, rates doubled/tripled — some pay $8k+ on $400k homes. Citizens Insurance (state backup) is overwhelmed.

- Property taxes: No state income tax is great, but millage rates + rising values mean bigger bills.

- HOA/ flood insurance: Many communities require it — add $300–$1,000/month.

Graph showing Florida's unique pain (home prices vs income ratio — we're outliers):

My step-by-step calculator for 2026 Florida reality:

- Gross monthly income × 28% = max housing payment.

- Subtract taxes (~1–1.5% home value/year), insurance ($500–$1,000/month average), HOA.

- Remaining = mortgage payment — back into price at current rates (6–7%).

- Add 20% down to avoid PMI.

Example: $80k household income ($6,667/month). 28% = $1,867. Subtract $600 taxes/insurance/HOA = $1,267 mortgage. At 6.5% rate = ~$200k loan (~$250k home with 20% down). Feels low compared to median $450k prices? Exactly — many stretch and regret.

Affordability infographic (the 28/36 rule updated for Florida extras):

:max_bytes(150000):strip_icc()/twenty-eight-thirty-six-rule.asp_final-8aea4a4d663140c1865477bb578fcddd.png)

My prediction for 2026–2027? Rates might dip to 5–6% if Fed cuts more, boosting buying power. But insurance reforms are slow — expect costs to stay high or rise with storms. Inventory is improving (more builds in Cape Coral), so prices could cool 5–10%. Best bet: Buy what you can truly afford (stress-test for 8% rates + $1k insurance).

The dream is possible (what smart buying looks like):

What's your affordability number? Dreaming of a Florida home but worried about costs? Share your income range or biggest concern in the comments — let's figure it out together!

Important Disclaimer This is my personal take for educational purposes only. I'm not a real estate or financial advisor. Home buying involves risks — consult professionals for your situation.

Follow me on X @MoneyWise2026

Angel from Florida

Comments

Post a Comment